Medicare Advantage is undergoing permanent structural changes driven by rising healthcare costs, increased use of AI, tighter provider networks, and stricter federal oversight. While many plans still advertise low or $0 premiums and extra benefits, hidden cost-shifting is causing millions of seniors to pay far more out of pocket than expected. Understanding these changes is now essential to avoid costly mistakes.

Why So Many Seniors Are Rethinking Medicare Advantage

For years, Medicare Advantage was marketed as the smarter alternative to Original Medicare. The appeal was obvious: low or zero monthly premiums, bundled prescription drug coverage, and extra perks like dental, vision, hearing aids, fitness memberships, and meal delivery.

For retirees living on fixed incomes, it felt like a financial win.

But across the United States, something has shifted. Seniors are increasingly reporting unexpected medical bills, denied services, and difficulties accessing the doctors they trust. Many are asking the same question: “Am I actually paying more than I should?”

This isn’t fear-mongering. It’s the result of real structural changes in how Medicare Advantage plans are designed, managed, and enforced.

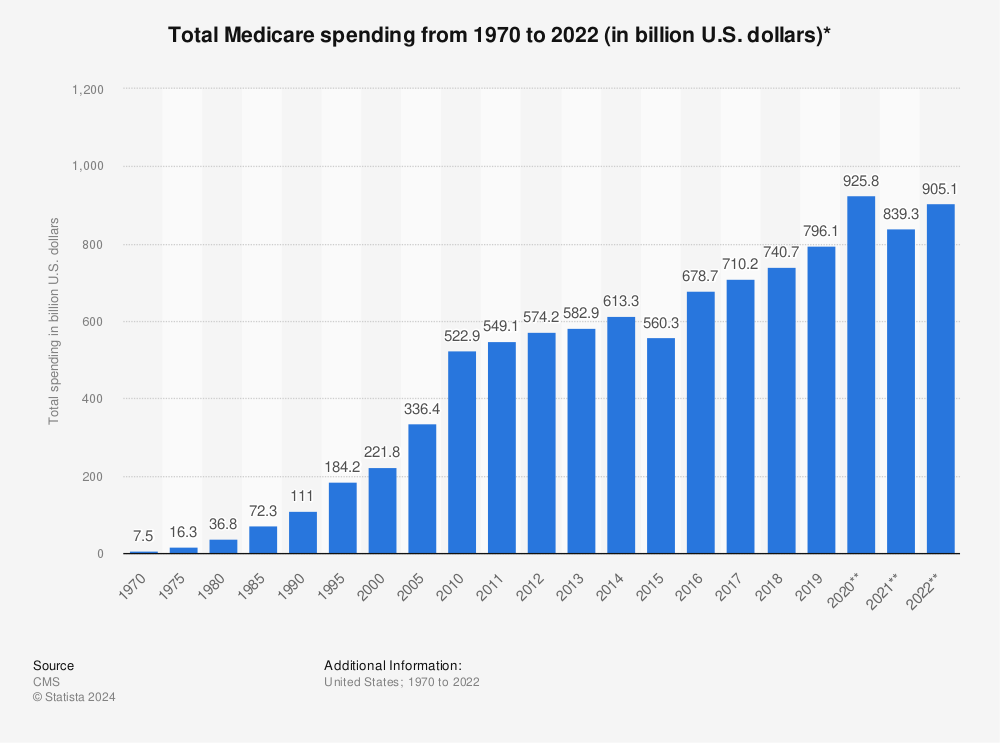

Enrollment data from the Centers for Medicare & Medicaid Services (CMS) shows that Medicare Advantage now covers more than half of all Medicare beneficiaries. When a system this large changes, the impact is widespread—and often confusing for those inside it.

What “Medicare Advantage Is Changing” Really Means

Medicare Advantage isn’t disappearing. Instead, it’s evolving in ways that fundamentally affect costs, access, and decision-making.

Several forces are driving this transformation:

-

Rising hospital, drug, and specialist costs

-

An aging population with more chronic conditions

-

Greater reliance on automation and AI

-

Increased federal scrutiny of plan behavior

-

Pressure on insurers to control spending

The result is a system that still looks affordable on the surface but operates very differently once care is needed.

Understanding these changes is the key to knowing whether you’re overpaying.

The Most Dangerous Myth: “Low Premium = Low Cost”

One of the most common misunderstandings about Medicare Advantage is that a low or $0 premium means the plan is cheap.

In reality, premiums are only one piece of the puzzle.

Medicare Advantage plans often recover costs through:

-

Copays for primary and specialist visits

-

Coinsurance for imaging, procedures, and hospital stays

-

Daily hospital charges after admission

-

Prescription drug tier pricing

Real-life example:

A 72-year-old retiree in Nevada enrolled in a $0-premium Medicare Advantage plan. During the year, she needed outpatient surgery, follow-up imaging, and physical therapy. By December, her out-of-pocket costs exceeded $6,000—nearly the plan’s maximum.

The plan wasn’t “bad.” It just wasn’t designed for someone who needed frequent care.

How AI and Automation Are Quietly Reshaping Medicare Advantage

One of the least visible—but most impactful—changes in Medicare Advantage is the increased use of automated decision systems.

Plans now rely on algorithms to:

-

Trigger prior authorization

-

Flag high-cost treatments

-

Predict recovery timelines

-

Review claims and appeals

These systems are promoted as efficiency tools, but they often create additional barriers for beneficiaries.

Real-life example:

A Medicare Advantage enrollee in Ohio was approved for short-term rehab after a hospital stay. After ten days, coverage stopped—not because her doctor recommended discharge, but because an automated system predicted recovery should already be complete. She appealed and won, but only after delays and stress.

Technology isn’t denying care outright—but it is deciding when care gets questioned.

Why Provider Networks Are Getting Smaller

Another permanent shift in Medicare Advantage is tighter provider networks.

To manage costs, plans are increasingly:

-

Dropping higher-cost hospitals

-

Limiting specialist availability

-

Steering patients toward preferred providers

This may not matter much if you’re healthy. It matters a lot if you’re not.

Real-life example:

A senior in Florida learned her longtime orthopedic specialist was no longer in-network after her plan updated its directory. Staying with the doctor meant higher costs. Switching meant delays and starting over.

Network changes rarely make headlines—but they reshape access quietly.

Prescription Drug Coverage: The Hidden Cost Accelerator

Medicare Advantage plans usually include Part D drug coverage, which many seniors see as a benefit. But formularies are becoming more restrictive.

Plans increasingly use:

-

Higher tiers for common medications

-

Step therapy requirements

-

Prior authorization for drugs once freely covered

Real-life example:

A beneficiary managing high blood pressure and diabetes saw two medications moved to higher tiers during annual plan updates. Monthly drug costs rose from $60 to nearly $220—without any change in treatment.

Drug coverage changes are one of the fastest ways costs increase without obvious warning.

Why Medicare Advantage Is Under Heavier Government Scrutiny

Federal regulators are paying closer attention to Medicare Advantage, particularly around marketing practices, denials, and risk coding.

The U.S. Department of Health and Human Services (HHS) has increased audits and enforcement actions targeting:

-

Improper denials of medically necessary care

-

Misleading plan advertisements

-

Inflated risk scores used to boost payments

While this oversight is meant to protect beneficiaries, it also pushes insurers to tighten utilization controls—often affecting member experience.

Who Is Most Likely to Overpay in Medicare Advantage?

Medicare Advantage doesn’t affect everyone equally.

You may be more likely to overpay if you:

-

Have multiple chronic conditions

-

See specialists frequently

-

Require rehab, therapy, or skilled nursing

-

Take several brand-name medications

-

Don’t review plan changes annually

Ironically, the people who rely on Medicare the most often experience the most friction.

Medicare Advantage vs Original Medicare: The Real Cost Trade-Off

There is no universal “better” choice—only better alignment with your needs.

Original Medicare typically offers:

-

Broad provider access

-

Fewer prior authorizations

-

Greater predictability

Medicare Advantage often offers:

-

Lower upfront premiums

-

Extra benefits

-

Cost controls that activate during illness

Analyses by the Kaiser Family Foundation (KFF) show that beneficiaries with higher healthcare needs often face more out-of-pocket spending under Medicare Advantage than they expected.

How to Tell If You’re Paying Too Much Right Now

Many seniors don’t realize they’re overpaying until after the damage is done.

Warning signs include:

-

Frequent prior authorization delays

-

Rising copays year after year

-

Losing access to trusted doctors

-

Hitting the plan’s out-of-pocket maximum

-

Avoiding care due to cost uncertainty

If these sound familiar, your plan may no longer fit your health reality.

What You Can Do to Protect Yourself

You don’t have to abandon Medicare Advantage—but you do have to stay proactive.

Smart steps include:

-

Reviewing the Annual Notice of Change (ANOC) every year

-

Comparing total out-of-pocket costs, not just premiums

-

Checking provider networks and drug formularies annually

-

Confirming doctors are still in-network

-

Using State Health Insurance Assistance Programs (SHIPs)

-

Reassessing your plan every Open Enrollment

Medicare is not a one-time decision. It’s an annual one.

Why These Changes Are Permanent, Not Temporary

The uncomfortable truth is that Medicare Advantage is changing forever.

AI-driven utilization management, tighter networks, and cost-shifting aren’t short-term trends. They are long-term responses to rising healthcare costs and demographic pressure.

Plans will continue advertising affordability. But affordability increasingly depends on how much care you actually need.

Frequently Asked Questions (Trending in the U.S.)

1. Is Medicare Advantage getting worse?

Not worse for everyone, but more restrictive for people with complex medical needs.

2. Are $0 premium Medicare Advantage plans really free?

No. Costs often appear later through copays, coinsurance, and drugs.

3. Why are more services requiring prior authorization?

Plans use utilization controls to manage rising healthcare costs.

4. Can I switch back to Original Medicare?

Yes, but Medigap access may be limited depending on timing and state rules.

5. Are Medicare Advantage denials increasing?

Audits and reports suggest denials and appeals are rising.

6. How do I know if my doctors are still in-network?

Check plan directories annually and confirm directly with providers.

7. Is Medicare Advantage cheaper than Original Medicare?

Sometimes, but not always—especially for high-need beneficiaries.

8. What is the biggest hidden cost in Medicare Advantage?

Out-of-pocket expenses during serious illness.

9. Should healthy seniors avoid Medicare Advantage?

Not necessarily, but plans should be reassessed as health changes.

10. Where can I get unbiased Medicare help?

State Health Insurance Assistance Programs (SHIPs) offer free counseling.

Final Takeaway: Medicare Advantage Isn’t Ending—But the Rules Have Changed

Medicare Advantage is not going away. But the version many seniors signed up for years ago is not the same one operating today.

Low premiums and extra benefits still exist—but they come with more strings attached. For millions of Americans, the real question is no longer “Is Medicare Advantage cheap?” but “Is it affordable for someone like me?”

If you haven’t reviewed your plan recently, you may already be paying too much—without realizing it.

In today’s Medicare landscape, informed beneficiaries save the most.

Comments

Post a Comment